Workshop : S.A.P.S VI (21-23 Mars 2007)

Workshop : S.A.P.S VI (21-23 Mars 2007)

Workshop : S.A.P.S VI (21-23 Mars 2007)

Statistique Asymptotique des Processus Stochastiques VI

Asymptotical Statistics of Stochastic Processes VI

(Statistique Asymptotique des Processus Stochastiques VI)

Université du Maine, Le Mans, 21-23 March, 2007

Sponsors : Université du Maine, FR 2962 du CNRS Mathématiques des Pays de Loire, CUM,Ministère de l’Education nationale,Conseil Général de la Sarthe and Conseil Régional des Pays de la Loire

Workshop S.A.P.S VI

Participants

- Bosq Denis, Paris

- Cawston Suzanne, Angers

- Chiganski Pavel, Le Mans

- Dabye Ali, N’djamena

- Dachian Sergueï, Clermont-Ferrand

- Dalalyan Arnak, Paris

- De Gregorio Alessandro, Milano

- Dehay Dominique, Rennes

- Farinetto Christian, Le Mans

- Fukasawa Masaaki, Tokyo

- Gassem Anis, Paris

- Golubev Youri, Marseille

- Gushchin Alexander, Moscow

- Hayashi Takaki, Keio

- Höpfner Reinhard, Mainz

- Iacus Stefano, Milano

- Khasminskii Rafail, Detroit

- Kleptsyna Marina, Le Mans

- Küchler Uwe, Berlin

- Kutoyants Yury, Le Mans

- Limnios Nicolaos, Compiegne

- Liptser Robert, Tel Aviv

- Lototsky Sergey, Los Angeles

- Lyasoff Andrew, Boston

- Malutov Mikhail, Boston

- Masuda Hiroki, Kyushu

- Mourid Tahar, Tlemcen

- Negri Ilia, Milano

- Nikulin Mikhail, Bordeaux

- Nishiyama Yoichi, Tokyo

- Privault Nicolas, Poitier

- Rabhi Anissa, Paris

- Shimizu Yasutaka, Osaka

- Tchirina Anna, Paris

- Vazquez Emmanuel, Gif-sur-Yvette

- Veretennikov Alexander, Leeds

- Vostrikova Ludmila, Angers,

- Yoshida Nakahiro, Tokyo

- Zaiats Vladimir, Barcelona

Presentation

Asymptotical Statistics of Stochastic Processes VI

(Statistique Asymptotique des Processus Stochastiques VI)

Université du Maine, Le Mans, 21-23 March, 2007

Sponsors : Université du Maine, FR 2962 du CNRS Mathématiques des Pays de Loire, CUM,Ministère de l’Education nationale,Conseil Général de la Sarthe and Conseil Régional des Pays de la Loire

The purpose of this workshop is to stimulate research in statistical inference for continuous time stochastic processes. This branch of mathematical statistics attracts more and more attention of the statisticians and probabilists because first : the real systems are often well described by the continuous time mathematical models (point processes, diffusion processes, stochastic differential equations with partial derivatives, stable processes etc.) and the second : the diversity of the models and the diversity of the statements of the statistical problems make these models quite attractive for the mathematicians because all these allow to obtain many new results which sometimes have no analogue in discrete time models.

Note that solutions obtained for continuous time models can be valid for discrete schemes of observation too. The computer realizations of the statistical algorithms (real data applications) requires that a special attention have to be payed to the effects due to discretization of continuous-time trajectories. Therefore, we wait that one (important) part of the talks will be devoted to statistical inference for discrete time observations (of continuous time systems).

Note as well, that statistical problems for stochastic processes are in the field of interests of the research teams of the universities of Rennes, Angers and Le Mans, hence this workshop can be considered as a current three-days seminaire triangulaire traditionally organized by these universities.

Scientific Programme Committee :

U. Küchler, Yu. Kutoyants, N. Yoshida.

Local Organizing Committee :

P. Chigansky, S. Dachian, A. Dalalyan, C. Farinetto, M. Kleptsyna, Yu. Kutoyants (Chair).

Program

SAPS VI

Program of 21, 22, 23 March 2007

Wednesday,

March 21

Morning session chair : R. HÖPFNER

Afternoon session chair : R. LIPTSER

|

10h00- 10h15 |

Opening | |

|

10h15- 10h50 |

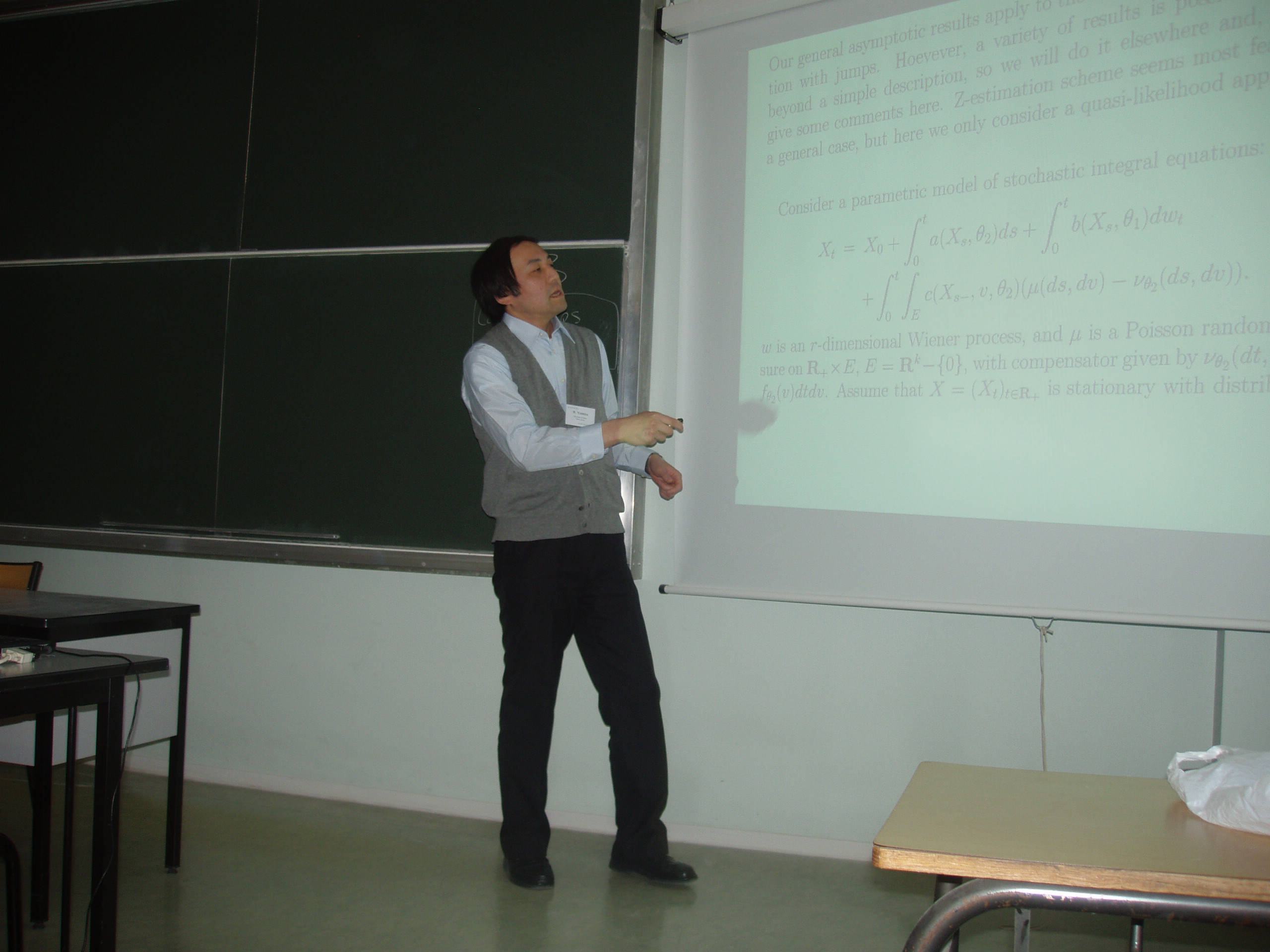

N. YOSHIDA (Tokyo). PLD and SDE with jumps. |

Slides (ps) |

|

10h50 - 11h25 |

A. DALALYAN (Paris) Second-order asymptotic expansion for the estimator of the covariance of two asynchronously observed diffusion processes |

Slides (pdf) |

|

Break | ||

|

11h35- 12h10 |

Y. GOLUBEV (Marseille) Ordered processes and high dimensional linear models |

Slides (pdf |

|

12h10- 12h45 |

S. LOTOTSKY (Los Angeles) Parameter estimation in stochastic partial differential equations |

Slides (pdf) |

|

Lunch | ||

|

14h30- 15h05 |

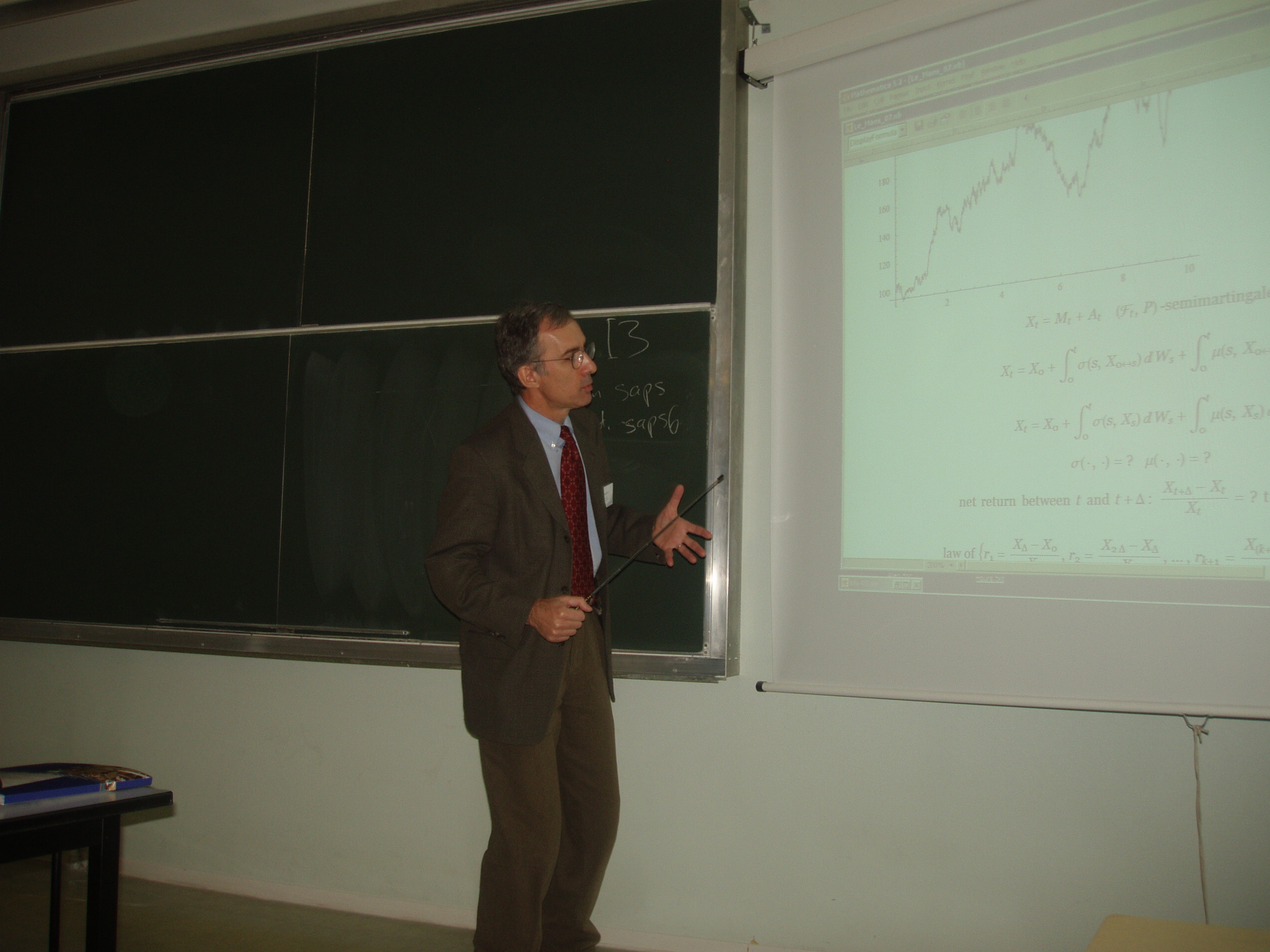

A. LYASOFF (Boston) Continuous time interpretation of discrete-time market data revisited |

Slides (pdf) |

|

15h05- 15h40 |

Y. SHIMIZU (Osaka) A practical approach to the inference for jump-diffusions from finite samples |

Slides (pdf) |

|

Break | ||

|

15h50- 16h25 |

M. FUKASAWA (Tokyo) Space discretized observation from continuous processes |

Slides (pdf) |

|

16h25- 17h00 |

R. HÖPFNER (Mainz) Estimating diffusion coefficient and drift in a set of neuronal data |

Slides (pdf) |

|

Break | ||

|

17h10- 17h45 |

S. IACUS (Milano) Estimation for the standard and geometric telegraph process |

Slides (pdf) |

|

17h45- 18h20 |

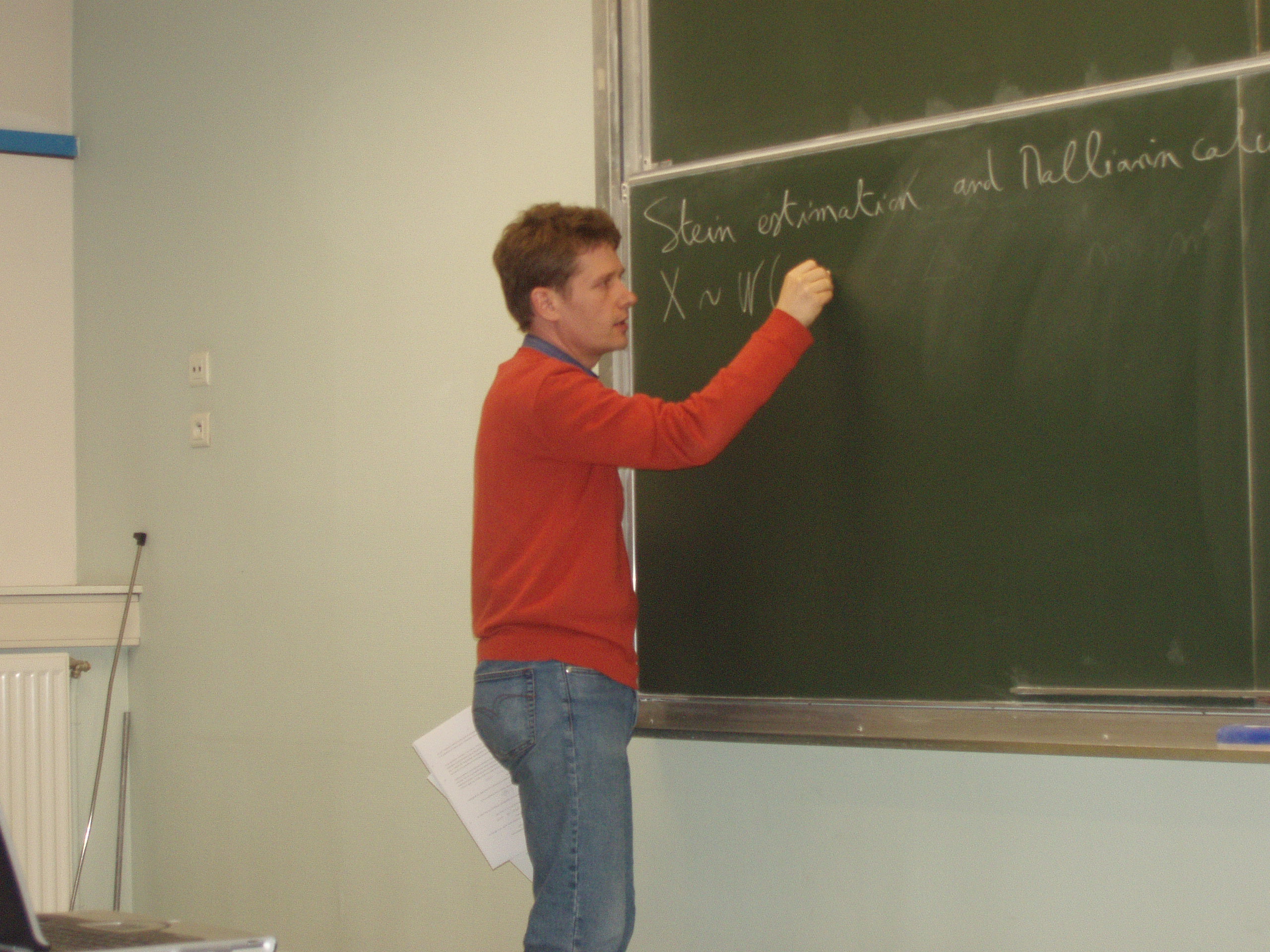

N. PRIVAULT (Poitiers) Stein estimation for the drift of Gaussian processes using the Malliavin calculus. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Morning session chair : M. MALYUTOV

Afternoon session chair : U. KÜCHLER

|

09h00-09h35 |

R. KHASMINSKII (Detroit) Filtering smooth signals for diffusion observed process |

Slides (pdf) |

|

09h35-10h10 |

P. CHIGANSKI (Le Mans) Filtering in strong noise |

Slides (pdf ) |

|

Break | ||

|

10h25-11h00 |

R. LIPTSER (Tel Aviv) Tracking volatility |

Slides (pdf ) |

|

11h00-11h35 |

A. VERETENNIKOV (Leeds) On Markov ergodic diffusion filtering in non-specified cases |

Slides (pdf) |

|

Break | ||

|

11h50-12h25 |

D. BOSQ (Paris) Adaptive projection estimation for a class of functional parameters |

Slides (pdf) |

|

Lunch | ||

|

14h30-15h05 |

T. HAYASHI (Keio) Nonsynchronous covariation with application to finance |

Slides (pdf) |

|

15h05-15h40 |

D. DEHAY (Rennes) Subsampling for non stationary processes |

Slides (pdf) |

|

Break | ||

|

15h50-16h25 |

Y. NISHIYAMA (Tokyo) Nonparametric estimation and testing time homogenity for Levy process |

Slides (pdf) |

|

16h25-17h00 |

M. MALYUTOV (Boston) On two discriminators between two classes of random processes |

Slides (pdf) |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Morning session chair : Y. KUTOYANTS

Afternoon session chair : N. YOSHIDA

|

09h00- 09h35 |

U. KÜCHLER (Berlin) News from sequential analysis for stochastic delay differential equations | |

|

09h35- 10h10 |

A. GUSHCHIN (Moscow) Parameter estimation for stationary solutions of stochastic delay equations |

Slides (pdf |

|

Break | ||

|

10h25- 11h00 |

T. MOURID (Tlemcen) Statistical problems on the number of delays in SDE |

Slides (pdf) |

|

11h00- 11h35 |

N. LIMNIOS (Compiegne) Nonparametric estimation in semi-Markov processes |

Slides (pdf) |

|

Break | ||

|

11h50- 12h25 |

M. NIKULIN (Bordeaux) Statistical analysis of failures of a redundant system with one operating unit and one stand-by unit in warm operating state |

Slides (pdf) |

|

Lunch | ||

|

14h30- 15h05 |

H. MASUDA (Kyushu) A simple estimator of a discretely observed stable process |

Slides (pdf |

|

15h05- 15h40 |

I. NEGRI (Bergamo) Asymptotical distribution free test for the drift of a diffusion process |

Slides (pdf) |

|

Break | ||

|

15h50- 16h25 |

S. DACHIAN (Clermont-Ferrand) Hypotheses testing for some point processes |

Slides (pdf) |

|

16h25- 17h00 |

Y. KUTOYANTS (Le Mans) On Goodness-of-Fit testing for continuous time processes |

Slides (pdf) |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}